Financial Spring Cleaning: A Smarter Reset for Your Wealth in 2026

/Financial Spring Cleaning: A Smarter Reset for Your Wealth in 2026

With Tax Day behind us, spring offers more than just a seasonal refresh, it’s an opportunity to bring clarity and intention to your financial life. For many high-net-worth individuals and families, complexity tends to build quietly over time. Multiple accounts, evolving tax laws, concentrated positions, and changing life priorities can all create friction if left unchecked.

Think of this as more than “cleaning”—it’s a strategic reset to ensure every element of your financial life is aligned, optimized, and working together.

Here are key areas to revisit this spring:

1. Look Beyond Your Tax Return—Identify Planning Opportunities

Your tax return is more than a record of the past—it’s a roadmap for future strategy.

Did your income shift into higher brackets or trigger phaseouts?

Were you impacted by recent tax legislative changes?

Did you capitalize on strategies such as tax‑loss harvesting, charitable planning, or retirement contributions?

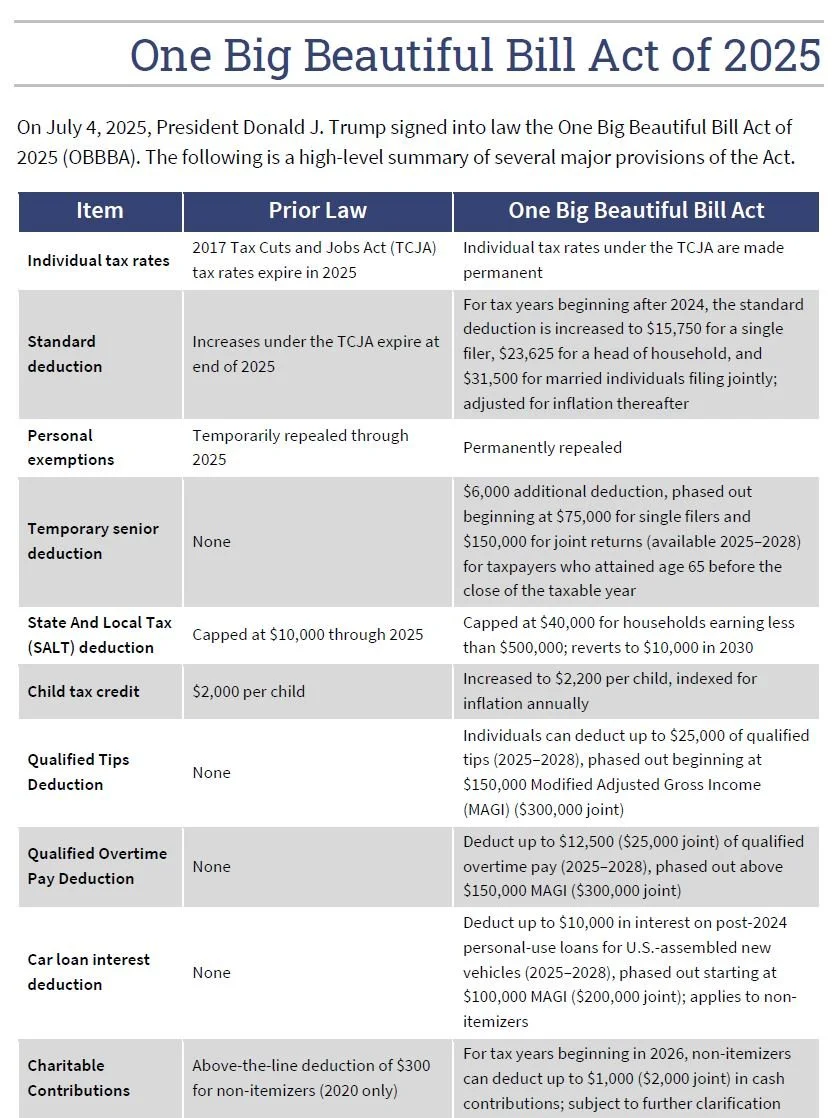

2026 Consideration: In light of significant changes to tax legislation, this is an ideal time to recalibrate forward‑looking strategies. Reviewing opportunities such as Roth conversions, donor‑advised funds, and the timing of income and deductions can help ensure your plan properly accounts for and capitalizes on the current tax environment.

2. Re-Align Your Financial Plan with Your Investment Strategy

One of the most common gaps we see: investments operating independently from the financial plan.

Has your risk tolerance shifted given market conditions or life changes?

Are your portfolios positioned in alignment with your long-term goals?

Are you coordinating tax strategy, cash flow, and investment decisions together?

At Gilbert & Cook, we believe investments should never exist in isolation—they are part of a dynamic, integrated plan designed to support your life.

3. Revisit Your Allocation—Including Private Markets & Alternatives

Public markets are only part of the opportunity set.

Are you overly concentrated in public equities or a single stock?

Have you explored access to private equity, private credit, or real assets?

Is your portfolio intentionally designed to balance liquidity needs today with long‑term investment opportunities?

2026 Consideration: Many sophisticated investors are continuing to expand into private markets for diversification, income generation, and long-term growth potential. Ensuring proper structure, pacing, and alignment with your liquidity needs is key.

4. Create Clarity Through Thoughtful Organization

Financial complexity often builds quietly not because the plan is flawed, but because life, wealth, and opportunities evolve.

Review and identify opportunities to consolidate legacy accounts, prior employer plans, and scattered custodians where appropriate

Centralize and organize critical documents (estate plans, tax returns, insurance policies) to support informed decision‑making

Review beneficiaries and account titling to ensure accuracy and alignment with your broader long‑term plan

A clear, well‑organized framework improves efficiency and strengthens coordination across your advisory team, allowing sophisticated strategies to work together intentionally and effectively.

5. Refresh Your Estate & Legacy Plan

Your financial life may evolve faster than your estate documents.

Have there been changes in family dynamics, wealth, or intentions?

Are your trusts, wills, and powers of attorney up to date?

Are you using tax‑efficient wealth transfer strategies for intergenerational planning?

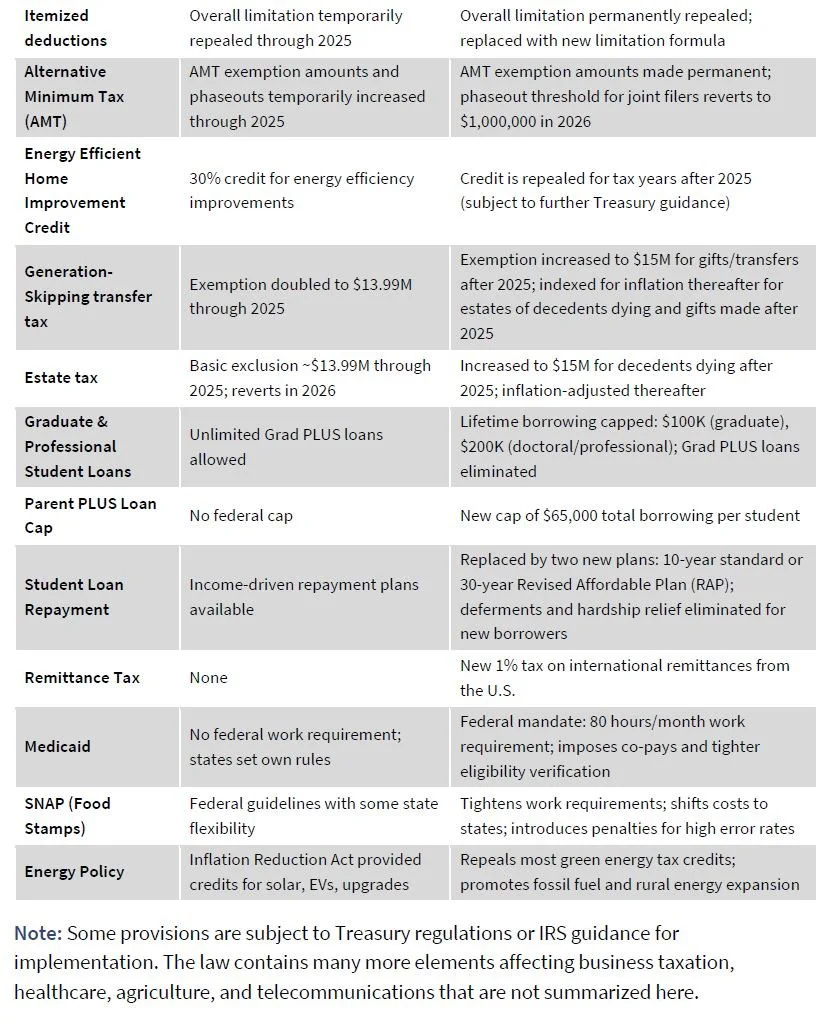

2026 Consideration: Elevated federal estate tax exemptions are now permanent under current law, offering a more stable planning environment. Although future legislative changes remain possible, today’s framework presents meaningful opportunities to optimize gifting strategies, trust planning, and long‑term wealth transfer. Revisiting your plan ensures it reflects both the current rules and your long‑term legacy goals.

6. Evaluate Cash Flow, Liquidity & Lifestyle Planning

Even for affluent families, cash flow planning remains critical.

Are you maintaining appropriate liquidity for near-term needs?

Have spending patterns shifted (travel, real estate, lifestyle upgrades)?

Are large upcoming expenses accounted for in your plan?

Spring is an ideal time to ensure your lifestyle and financial structure remain in harmony.

7. Strengthen Risk Management & Protection Planning

Wealth is not just built—it must be protected.

Review insurance coverage (life, disability, umbrella liability)

Assess cybersecurity and identity protection measures

Evaluate business owner risks or key-person exposure

As your balance sheet grows, so does the importance of protecting it.

8. Clean Up the “Invisible” Leaks

Even sophisticated investors accumulate inefficiencies.

Unused subscriptions or redundant services

Tax-inefficient accounts or investment placements

Idle cash not aligned with your strategy

Small inefficiencies, compounded over time, can meaningfully impact outcomes.

9. Reconnect with Your Advisory Team

The most valuable step may simply be a conversation.

At Gilbert & Cook, we often say that as your life grows more complex, your need for coordinated advice grows with it. Spring is an ideal time to reconnect, revisit your goals, and ensure your strategy reflects where you are today—and where you’re going next.

Final Thought: Create Space for What Matters Most

Financial spring cleaning isn’t about perfection—it’s about intention.